Economy

From interest rates to inflation, understand the impact of macroeconomic trends on the real estate capital markets.

The Beyond Insights series aims to deliver timely economic and market-driven insights to better inform your commercial real estate investment decisions.

Markets

From local market rents to cap rates, catch up on the latest capital markets insights.

Learn moreU.S. ECONOMIC MACRO COMMENTARY & INSIGHTS

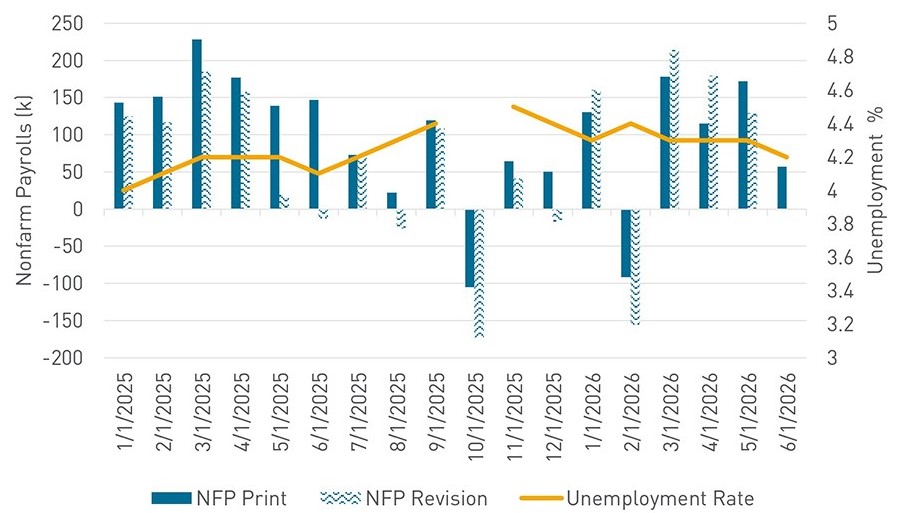

Labor Market Cools, but Inflation Remains the Bigger Problem

- June nonfarm payrolls increased by 57,000, well below expectations and accompanied by downward revisions to prior months.

- The unemployment rate declined to 4.2%, though much of the improvement was driven by a drop in labor force participation rather than stronger hiring.

- Hiring momentum has clearly moderated from the stronger pace seen earlier this year, but the data stops short of signaling a material deterioration in labor market conditions.

- Chair Kevin Warsh continues to emphasize incoming data over explicit policy guidance, increasing the market importance of each major economic release.

nonfarm payrolls print vs. revision

2026 Multifamily Investor Sentiment Survey

In December 2025, we surveyed over 250 of our trusted clients from various companies, with most holding senior-level titles, for our second annual Multifamily Investor Sentiment Survey. Our goal is to provide a comprehensive view of current market sentiments to our clients, and we plan to share our findings in our detailed report.

2026 Multifamily

Powerhouse Poll

In Berkadia’s Annual Multifamily Powerhouse Poll, we surveyed over 200 investment sales advisors and mortgage bankers to offer their unique perspectives on the state of the commercial real estate (CRE) industry.

Labor Market Cools, but Inflation Remains the Bigger Problem

After three consecutive months of stronger-than-expected payroll growth, June finally delivered a downside surprise. Employers added just 57,000 jobs during the month and prior months were revised lower, taking some of the shine off what had looked like a meaningful reacceleration in hiring. Headline unemployment rate improved to 4.2%, but the details were less encouraging.…

The Missing Dot

Everyone will focus on the missing dot. The market sold off because of the nine that remained. Half the committee is now willing to discuss another rate hike this year, and that is a very different conversation than the one markets were having just a few months ago. Inflation forecasts moved higher, growth forecasts moved…

Multifamily Lending Mid-Year Market Landscape

The key theme of the Commercial Real Estate (CRE) lending space to start the year was the abundance of liquidity. The Federal Housing Finance Agency (FHFA) raised the Agencies’ caps to $88B. Debt funds were abundant with multifamily-specific capital to lend, and life companies had fresh allocations. To start the year, the Agencies were competitive…