U.S. ECONOMIC MACRO COMMENTARY & INSIGHTS

Labor Market Cools, but Inflation Remains the Bigger Problem

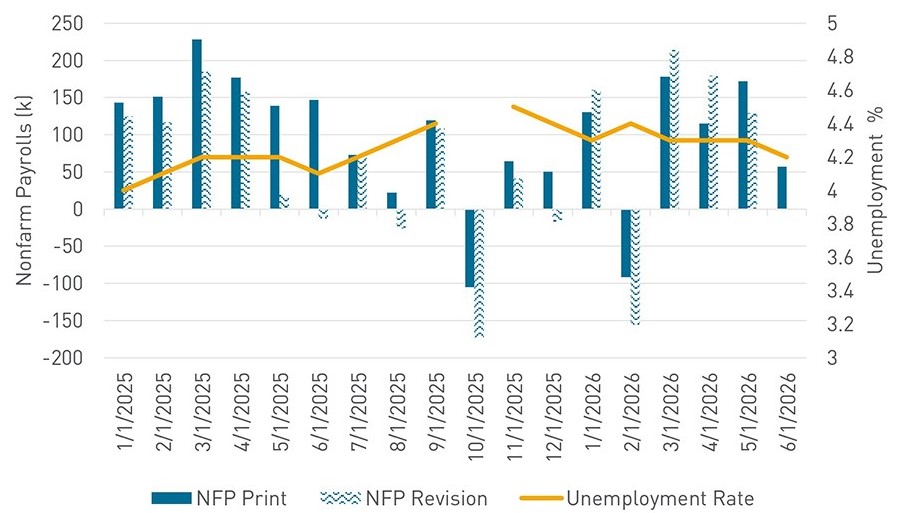

- June nonfarm payrolls increased by 57,000, well below expectations and accompanied by downward revisions to prior months.

- The unemployment rate declined to 4.2%, though much of the improvement was driven by a drop in labor force participation rather than stronger hiring.

- Hiring momentum has clearly moderated from the stronger pace seen earlier this year, but the data stops short of signaling a material deterioration in labor market conditions.

- Chair Kevin Warsh continues to emphasize incoming data over explicit policy guidance, increasing the market importance of each major economic release.

nonfarm payrolls print vs. revision

2026 Multifamily Investor Sentiment Survey

In December 2025, we surveyed over 250 of our trusted clients from various companies, with most holding senior-level titles, for our second annual Multifamily Investor Sentiment Survey. Our goal is to provide a comprehensive view of current market sentiments to our clients, and we plan to share our findings in our detailed report.

2026 Multifamily

Powerhouse Poll

In Berkadia’s Annual Multifamily Powerhouse Poll, we surveyed over 200 investment sales advisors and mortgage bankers to offer their unique perspectives on the state of the commercial real estate (CRE) industry.

Beyond Insights: Markets

From occupancy to cap rates, employment to migration trends, read the latest market-driven insights.

BOMA Healthcare Conference Recap

The Graying Gold Rush: Seniors Housing Outshines Amid Uncertainty

Private Credit in CRE: Liquidity, Competition, and Evolving Opportunities in 2026

MBA CREF 2026: Five Takeaways Shaping CRE Lending & Investment

The Forum at Sam Houston, Huntsville, TX | Sold and Financed by Berkadia 2026

Berkadia Negotiates Student Housing Property Sale in Huntsville, Texas Huntsville, Texas – July 22, 2026 – Berkadia, a distinguished leader in the commercial real estate sector, announced today the sale of The Forum at Sam Houston a 450-bed, garden-style student housing property in Huntsville, Texas. Senior Managing Directors Travis Prince and Kevin Larimer, along with…

Vibra Hospital of the Central Dakotas, Bismarck, ND | Arranged Equity and Financed by Berkadia 2026

Berkadia Arranges Equity Placement and Financing for Vibra Hospital of the Central Dakotas Development in Bismarck, North Dakota Bismarck, North Dakota – July 21, 2026 – Berkadia, a distinguished leader in the commercial real estate sector, announced today the equity placement and financing for the development of Vibra Hospital of the Central Dakotas, a 50-bed…

The Ambassador of Scarsdale, Westchester County, NY | Sold and Financed by Berkadia 2026

Berkadia Announces Sale & Financing of Trophy Senior Living Asset in Westchester County Scarsdale, New York – July 21, 2026 – Berkadia, a distinguished leader in the commercial real estate sector, announced today the sale and financing of The Ambassador of Scarsdale, a 121-unit Class-A assisted living and memory care community in Westchester County, New…