A question weighing on many multifamily developers’ minds is what the new landscape will look like for apartment development in Houston. Without a doubt, city officials will, at a minimum, review existing building codes and flood zones and make suggested changes to better cope with flooding hazards in the future. These changes could have a profound impact on development in some of the hardest-hit communities in Southwest Houston that border the riverways, most of which are vintage, garden-style workforce housing. Of the 66,000 units in this area, as much as 30 percent could be impacted by flooding.

In the immediate aftermath of a natural disaster, it’s important to remember early estimates of the damage are an inexact science and will most likely be revised; however, what we do know is that roughly 30,000 to 40,000 homes have been destroyed throughout the Houston area. Approximately 52 percent of residential and commercial properties are not located in federally designated flood zones, with the risk being that many of these structures lack comprehensive flood insurance. Officials are estimating that the extent of the damage will likely reach $160 billion, making Hurricane Harvey the most damaging hurricane in the country’s history.

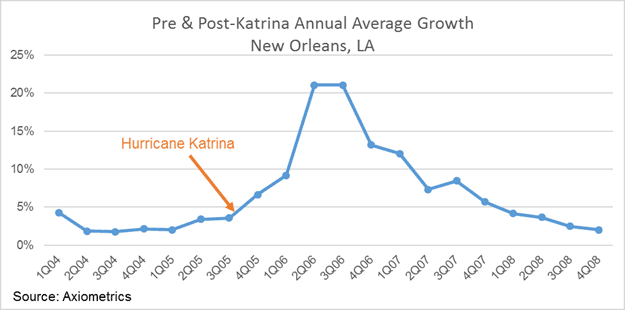

Though the full extent of the damage caused by Hurricane Harvey is still being estimated, we can draw parallels from the effect that Hurricane Katrina had on New Orleans to what the aftermath of Hurricane Harvey will look like for the multifamily market in Houston. Pre-Katrina, the New Orleans multifamily market had an inventory of approximately 48,000 units. The devastating flooding that Katrina wrought on New Orleans wiped out 24 percent of the metro’s multifamily stock. Houston’s overall multifamily stock of 637,000 units dwarfs New Orleans, but one thing is certain: if we see a similar proportion of Houston’s stock become functionally obsolete, a precipitous rise in average rent is right around the corner for Houston as displaced residents rush to secure livable housing units. As illustrated below, New Orleans experienced four consecutive quarters of annual rent growth of over 10 percent (two of which were over 20 percent) in the immediate aftermath of the storm. Ultimately, it will take some time to understand the full extent of the damage to Houston’s multifamily inventory, but according to CoStar, roughly 72,000 apartment units fall within the 100-year floodplain. Should the majority of those units be found to be unlivable, that would total over 11 percent of Houston’s apartment stock.

Similarities between New Orleans and Houston in the wake of each metros respective disaster begin to diverge when discussing post-disaster development. New Orleans and Houston are two very different markets. Whereas New Orleans is a regional market, Houston stands as a top-five market historically for multifamily investment. Like New Orleans, developers in Houston will most likely see a rise in the cost of insuring their assets. But, whereas the groundswell of post-Katrina developers were local and entrepreneurial in spirit, often self-financing their acquisitions, it’s hard to imagine national developers shying away from the country’s fifth-largest metro anytime soon.

Katrina showed what a storm of similar magnitude could do to the psyche of residents, with half of the greater New Orleans population fleeing. But it’s difficult to conceive of a similar situation playing out in Houston. Although the results from Berkadia’s servicing arm are preliminary, out of a total of 255 loans serviced in the Houston area, only 13 (5.1%) sustained damage over $25,000, and 45 (17.6%) had damage of less than $25,000. The Houston MSA is the sixth-largest economy among U.S. metro areas, and the epicenter of the oil and gas industry with over 4,800 energy-related establishments. In addition to pledging $10.3 million for disaster relief, ExxonMobil has affirmed they are undeterred in continuing to move employees to its brand-new, state-of-the-art campus in Springwood Village in the coming years. With economic anchors like the oil and gas industry, financial services industry, the Port of Houston, and Johnson Space Center, the Houston economy is too dynamic and full of opportunity to envision similar population and job losses.

For more commentary, see Ryan Epstein and Tucker Knight’s insights in Hurricane Harvey’s Multifamily Impact | Multi-Housing News