Coming off the heels of the Global Pandemic, residential housing went on a record runup in prices from the start of 2021 through the first half of 2022. However, the Federal Reserve’s interest rate hike campaign steadily slowed price growth. This marked an end of peak pricing (July ’22), leading to a sharp decline in transaction volume in Q3 2022 and a near halt to wrap up Q4 2022. While many of the macroeconomic themes carried into 2023, so did new challenges in recent months initiated by rising interest rates, –falling homes prices, and banking sector turmoil.

Nevertheless, the residential housing sector—single-family rentals and build-to-rent remained resilient compared to other sectors of commercial real estate such as office and multifamily. Residential traditionally has been, and still is widely considered, a relatively safe investment as people will always need a place to live. Since the last financial crisis, the increased pricing and low yields within the multifamily industry have led investors to single-family rentals and build-to-rent due to higher overall returns. As we have passed the half-way point of 2023, we will explore the emerging trends, statistics, transactions, and outlook of this burgeoning segment in the real estate sector – Single-Family-Rentals (SFR) and Build-to-Rent (BFR).

Single-Family & Build-for-Rent Communities

Single-family rentals and build-to-rent communities have witnessed remarkable growth and performance in recent years attracting strong investor and resident interest alike. The sector’s success can be attributed to several key factors nationally including rising demand for rental housing, lack of home ownership affordability, resiliency in slowing markets, and long-term investment potential in consistently appreciating markets. With SFR & BTR officially dubbed as its own asset class, we expect this sector to continue serving as a convenient alternative asset class. It caters widely to a range of real estate professionals.

How Investors View the Market

Investor appetite and the deployment of capital into the marketplace through the first half of 2023, has been a completely different story from the second half of 2022. Contrary to the second half of 2022, we are no longer exclusively in a “Private Capital/Family Office” buyer pool environment. Not only did we see a decent percentage of institutional investors return, we saw a consistent increase in the overall buyer pool. As capital gets back to work, the numbers are up on all fronts from executed confidentiality agreement (CA) count, property tours and offers submitted. Our recent build-to-rent listings are again experiencing double-digit tours and offer counts. That doesn’t necessarily mean the overall price of an asset is increasing, but the increased competition is certainly allowing more favorable results for the seller. Additionally, we are starting to see the revival of “Risk Adjusted Returns” and “location, location, location,” as we are getting back to basics again.

Investors returning to the market today are often not overly focused on the short-term outlook (one to two years), rather they are focused on the long-term outlook (three-ten+ years). The investors returning to the market see that the underlying fundamentals driving residential housing are exceptionally strong. To further explore, we will showcase three recent assignments that the Berkadia SFR/BFR Team has transacted on:

Berkadia PHX Office Sale Highlight

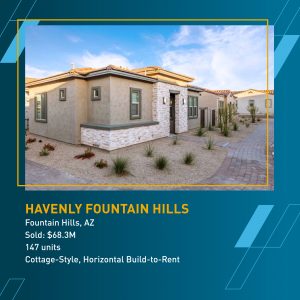

Havenly Fountain Hills (147 Units) – Fountain Hills, AZ

Product Type:

- Cottage-Style, Horizontal Build-to-Rent (One (1) APN #)

- 1-, 2- & 3-Bedroom Units (Avg. SF – 1,023)

Built by Keystone Homes “Havenly Fountain Hills”, consists of 147 units and falls under what we call the “Horizontal-Multi or Cottage-Style” Build-to-Rent Sector. The property is located in Fountain Hills, Arizona, a “Top Baby-Boomer” retirement destination in the country. The submarket has a very low existing apartment and rental home stock base, with a small future construction pipeline of less than 400 units. The high barriers to entry in the submarket, coupled with a strong resident demographic profile, and over $ million homes on average, increased investors’ appetite for the asset, even with a volatile interest rate environment for financing.

With the negative economic headlines, it was important to get the buyer pool of the asset to understand the supply and demand story, quality of the asset, and resident profile to drive a strong result. However, as the 10-Year Treasury continued to fluctuate daily, financing has been a challenge to say the least. Berkadia Mortgage Banking experts based out of Scottsdale used their Life Company relationships to lock in a crucial Rate Lock, much earlier than typical financing can occur with Agency financing.

During the pandemic boom (2021 – 2022), we saw Horizontal Cottage-Style Cap Rates trading between 2.9 percent to 4.0 percent, with Arizona peak sale pricing reaching $484,000 per unit. If we compare Havenly Fountain Hills trading at an in-place cap rate of 5.0 percent and a sales price of $464,000 per unit, the seller received a tremendous outcome. Higher than the original proforma projections, with the buyer receiving an exceptional Trophy-Asset yielding better than historical norms. Not to mention, if built the year prior, this asset would have traded in the low $700,000 per unit range, with a 3 percent cap rate.

In the next section, we will explore the recent sales transactions from the Southwest Region of two Build-to-Rent communities by the Nation’s largest home builder. Both properties are purpose-built rental subdivisions comprised of three- and four-bedroom homes with two-car attached garages. As home values across the country decreased from their highs, savvy investor interest was still actively seeking out investment opportunities. One major contributing factor is the usually stable rent and predictable cash flow of the single-family rental and build-to-rent asset class. During the Great Financial Crisis of 2007-2009, home prices decreased nationally, and yes rent growth diminished as well, but rents as whole never went “negative” through that period.

Berkadia National Sale Highlight

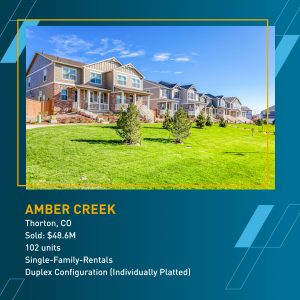

Amber Creek (102 Homes) – Thornton, Colorado

Product Type:

- Single-Family-Rentals – “Duplex Configuration (Individually Platted)”

- 3- & 4-Bedroom Homes

As the country came out of the Great Financial Crisis, strict lending criteria and burdensome debt forced builders to deliver homes under the allocated permits and demand amount. In simple terms, certain markets across the country built well below permit levels from 2009 – 2019. Even after the Post-Pandemic Boom, 2021 – 2023, consulting experts continue to reference that the country is short on housing between estimates of 3.5 – 6.5 million homes. In the case of Amber Creek, the strong product offering & high barriers to entry submarket of Thornton, Colorado led to an extremely well executed result of 30 + Tours and 30 + Offers.

Berkadia Regional Sale Highlight

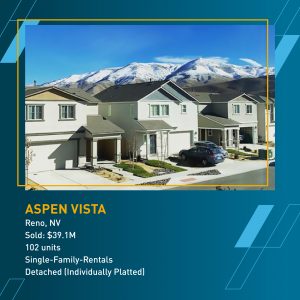

Aspen Vista (102 Homes) – Reno, NV

Product Type:

- Single-Family-Rentals – “Detached (Individually Platted

- 3- & 4-Bedroom Homes

To compare the asset values of purpose-built rental subdivisions during the Pandemic-Boom of 2021, versus Post-Boom today we explore the inverse scenario of the “Residential Housing Income-Stream” in the capital markets. In 2021, we could sell the “Income-Stream” of the rental subdivision anywhere from 10 percent- 60 percent higher than what the “Retail” Home was selling for across the street.

- Relatively Risk-Free Debt between a 3 percent – 4 percent rate, allowed institutional investors to out compete “retail buyers” on a bulk scale.

- Conversely today, as Debt is +/- 5.5 – 6.0 percent, investors and institutions are capped by their minimum net yield requirements, thus allowing the “Retail” buyer to outcompete an institution. The personal budget of a retail buyer allows them to stretch pricing versus a minimum net yield by the institutions.

In summary, transactions are still getting done today, however, they take a little more effort by an experienced brokerage team and more financial engineering. If you don’t have to sell in today’s market, improving overall operations of the asset in preparation of a future sale may yield the best outcome in today’s current environment.

Emerging Trends:

- Wallet Factor coming off the global pandemic, high inflation, and record consumer debt levels give many renters a strong incentive to stay put and save money. Conversely, as supply-side pressure grows, residents can competitively shop rental housing options if they are looking to save even $100/month as small dollar savings add up.

- Joint Venture Equity providers are shifting strategies to Preferred Equity to mitigate risk.

- Institutional single-family rental operators will continue to recycle older properties out, while replacing stock with new build construction, and fresh acquisitions.

- Big home builders’ market-share will continue to grow as fewer homes are being built by smaller builders, regional and local who need construction loans. Regional Banks are reducing lending. They now require more equity & charge higher lending rates.

Regional News:

- Southwestern Cities that rank in the “Top 20 Metros with the Most SFR Units Under Construction” – Phoenix Ranks #1 (+/- 5,500 Units), Salt Lake City #9 (+/- 1,000 Units), Denver #13 (+/- 900 Units), Las Vegas #16 (+/- 650 Units)

- Empire Group receives $78.5 million in non-recourse bridge financing for “Village at Pioneer Park”, a 332-unit build-to-rent community in Peoria that was recently completed & $42 million in non-recourse financing for “Village at Skyline Ranch”, a 167-unit BTR community currently under development near Luke Air Force Base in Glendale.

- Rockefeller Groups acquires two sites in Phoenix’s South Mountain Corridor for the development of 152 Build-to-Rent “Townhome” Units. Groundbreaking scheduled for Summer 2023, with deliveries starting in Q1 2025. Development scope ranges from 1,100 – 1,500 Unit Sqft., with two- & three-bedrooms.

- Poplar Homes enters the Arizona marketplace with the acquisition of Venture REI’s single-family-for-rent property management portfolio adding 152 Homes in Scottsdale, AZ as part of its national expansion efforts.

- Shopoff Realty Investments and the Urban Pacific Group of Companies have created a joint venture partnership to further advance Urban Pacific’s Urban Town House (UTH) build-to-rent, multi-generational housing concept.

National News:

- Pretium Partners LLC, struck a 4,000 Home direct deal with R. Horton, Inc. valued at more than $1.5 Billion.

- Invitation Homes nears a deal for 2,000 Starwood Rentals, sources close to the deal note that homes are within the Sunbelt markets of “Atlanta, Houston, Phoenix, and Tampa)

- Sculptor Real Estate boosts Second Avenue’s SFR investments. Joint Venture brings addition of 500 Homes, $100 million in capital.

- Senators File a Bill to Undercut SFR Institutional Investment: “A number of democratic senators are looking to eliminate extensive institutional investment in single-family rentals. Senators Sherrod Brown (D-Ohio), Ron Wyden (D-Ore.), and others introduced a bill called the “Stop Predatory Investing Act”” (Globestreet.com, Erik Sherman – 7/13/23)

- Insurance Costs continue to rise throughout the United States: “The National Multifamily Housing Council released its Multifamily Risk Survey and Report this week, which showed respondents are experiencing property insurance costs that are 26% higher than they were last year.”

Outlook:

- Pullback in construction lending and starts may create a major hole in supply by 2025+.

- Supply-side pressure grows for both multifamily and SFR/BTR: As more supply is delivered to the market, submarkets will continue to see competitive lease-up scenarios. Strong operations are a must in today’s environment. Prospective renters have more options to choose from today 2023 – 2025 than in the pandemic 2021 – 2022.

- Investors who have studied this space over the past –three to five years have now entered the market, a trend that we expect to significantly increase in the coming years. We expect the cross pollination of the buyer pool to continue. Traditional multifamily investors are buying “Rental Subdivisions,” conversely institutional single-family rental operators are entering the “Cottage-Style” sector.

- Demographic and generational trends will continue to make buying a home difficult; Berkadia expects both short-term and long-term tailwinds to be optimistic, even amongst investor and economic uncertainty.

- Strong in-migration patterns, and job growth will continue throughout the Sunbelt, Mid-Atlantic, and Mountain Region, which is where new net demand of housing is occurring the most.

- Consolidation between single-family rental operators, Home Builders, and build-to-rent

- Developers will pick up through the end of 2023, heading into 2024.

About Berkadia’s National Single-Family Rental and Build-to-Rent Platform:

Berkadia has been recognized by its peers and industry experts taking home the Inaugural 2022 Single-Family Rental Industry Investment Sales & Debt “Brokerage of the Year.” This award was presented at IMN’s established 10th Single-Family Rental Investment Conference in Scottsdale, Arizona.

As demand for the sector has increased significantly, many investors are shifting their investment strategies to include Single-Family Rental (SFR) and Built-to-Rent (BTR). Berkadia’s national footprint, with unrivaled local expertise, has never been more valuable, leading the firm to record-breaking production volume of $4 billion, with YTD 2022 volume in excess of $1 billion.

We’re grateful for all our clients, peers, partners, and friends who have supported us in this journey. We look forward to our continued success together in 2023!