Q1 2022 — Multifamily posts strongest return since 1980 amid a contracting economy and high inflation

In the first quarter of 2022, the one-year compound return for U.S. multifamily real estate reached the highest level since 1980 — clocking in at over 24%.

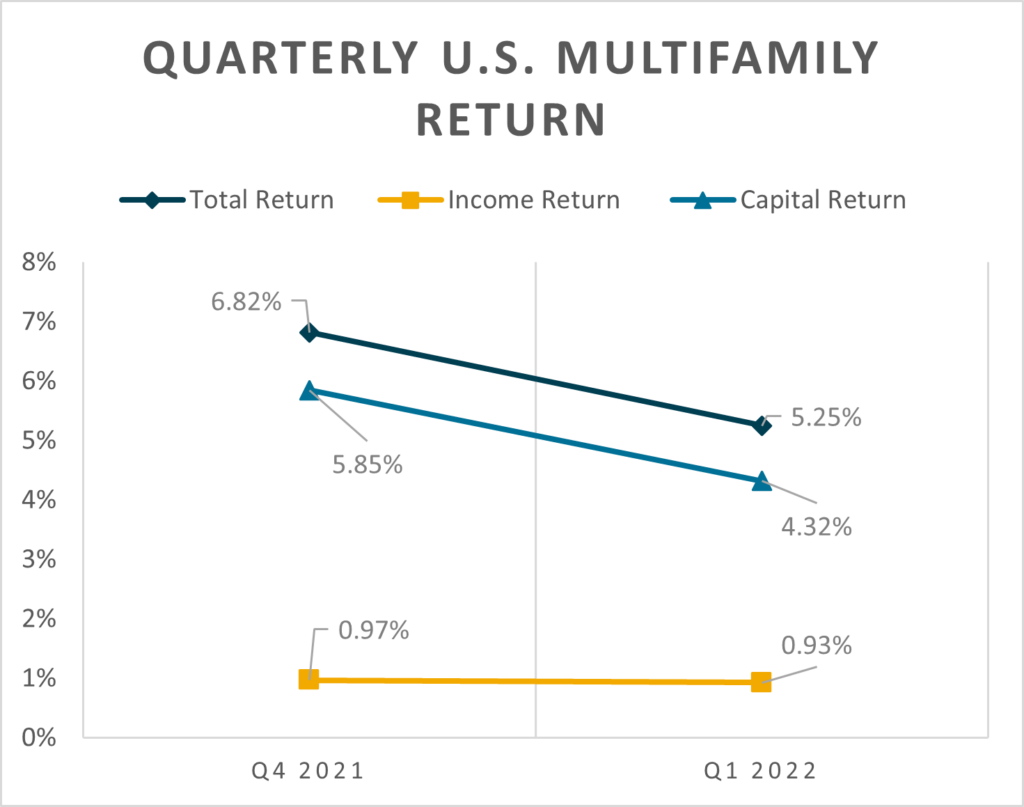

What’s the story behind this stunning growth? Simply put, appreciation returns have been consistently strong over the past four quarters. Quarterly income and appreciation (capital) returns dropped relative to last quarter, so the 24% was not driven by disproportionately large quarterly returns in the first quarter of 2022.

Source: National Council of Real Estate Investment Fiduciaries (NCREIF)

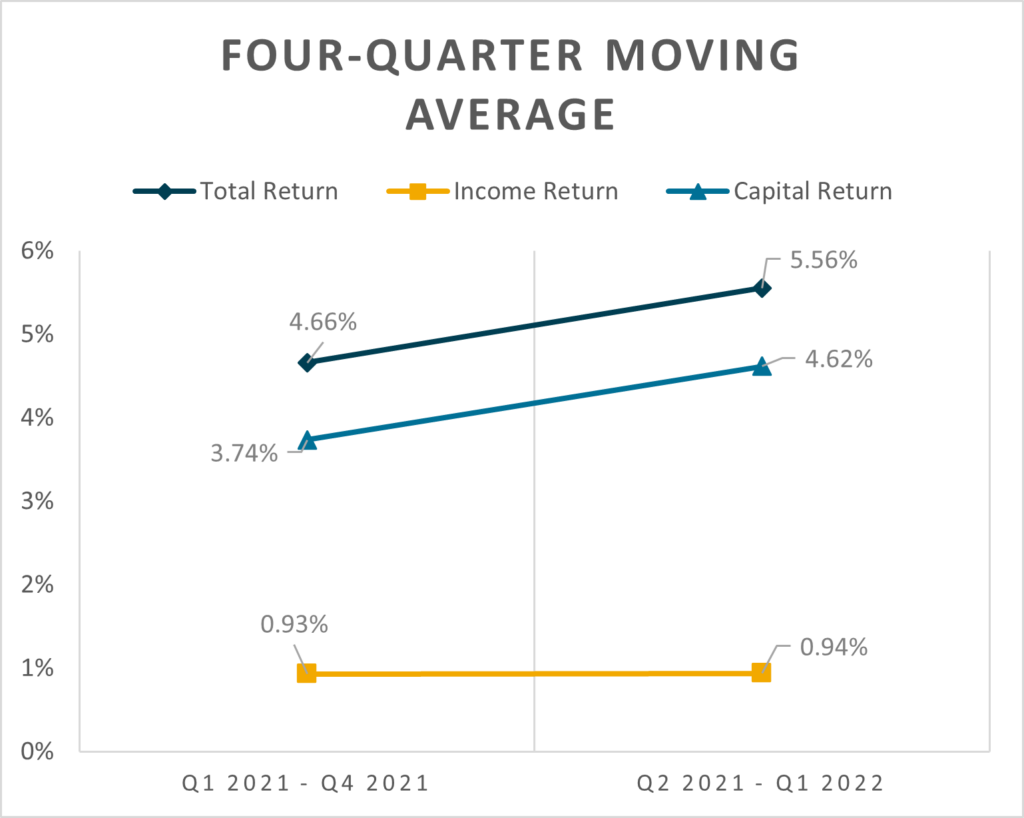

Rather, the main driver was the rise in the average appreciation return over the past four quarters.

Source: National Council of Real Estate Investment Fiduciaries (NCREIF)

From 1Q21 to 4Q21, quarterly appreciation returns looked like this:

Q1 2021 | 0.79%

Q2 2021 | 2.71%

Q3 2021 | 5.59%

Q4 2021 | 5.85%

And from 2Q21 to 1Q22, they looked like this:

Q2 2021 | 2.71%

Q3 2021 | 5.59%

Q4 2021 | 5.85%

Q1 2022 | 4.32%

Notice that moving from the former to the latter window, we drop our consideration of the 0.79% quarterly appreciation return and replace it with 1Q22’s 4.32% return. So, even though 1Q22’s appreciation return declined relative to last quarter’s 5.85%, the combination of returns over the past year yielded a higher one-year compound appreciation return and therefore a higher one-year compound total return. The other component of the total return — the income return — has been rather flat, so its effect is not worth considering.

Multifamily performed very well in a quarter largely characterized by a contracting U.S. economy and high inflation. In the first quarter of 2022, the U.S. economy contracted by an annual 1.4%, and inflation ran at an average of 8%. Investors continue to favor multifamily real estate driven by strong underlying fundamentals. During the same time, the national occupancy rate for multifamily product stood at 98%, while effective rent grew at an annual rate of 16%. In essence, real estate owners have been able to increase future cash-flows, resulting in positive capital appreciation. Thus, such observations confirm our assessments in ‘Real Estate in Context: Interest Rates, Stagflation, Inflation, and Monetary Policy.’ Our research suggests that multifamily real estate is highly resilient and truly outperforms during times of ‘quasi-stagflation’ or periods of high inflation and suboptimal economic growth.

We at Berkadia will continue monitoring the situation and encourage your reaching out to us to learn more.