U.S. ECONOMIC MACRO COMMENTARY & INSIGHTS

- Mortgage rates reverse path and spoil the fall buying season

- Home sales remain stagnant

- Renting remains financially advantageous for many

Just four short weeks ago, the outlook for single-family land was rosy. Treasury rates had rallied, and 30-year mortgage rates had fallen to their lowest level in two years, almost breaking through into the high 5% range. The jumbo-sized, 50-basis-point rate cut by the Fed had first-time buyers salivating over a relief rally, and even moved some tentative homeowners into the sell category. Unfortunately for those prospective buyers, rates have since reversed course and the fickle market has adjusted its projections for future rate cuts, as recent labor market prints underpin the strength and resilience of the U.S. economy.

Activity in the single-family housing market is highly correlated to mortgage rates. Roughly 60% of homes in the United States carry a mortgage, and during the refinance boom and ultra-low-rate environment of the post-COVID years, nearly one-third of those outstanding mortgage balances were refinanced. According to Freddie Mac’s Primary Market Mortgage Rate Survey, the 30-year fixed-rate mortgage averaged 3.0% in 2021, during which time there was about $2.8 trillion in first lien refinance originations.

More than three-quarters of homes with a mortgage have rates below 5.0%, and that figure jumps to more than 85% if you raise the mortgage rate bar to 6.0%. Homeowners who are shackled with golden handcuffs to their low-interest-rate mortgages are hesitant to move despite the increased equity in their primary residence, as a new mortgage payment would represent a drastic increase thanks to higher borrowing costs. Presumably, transaction activity in “existing home” single-family land will remain muted until interest rates reach levels for borrowers that balance out the persistently high prices for homes.

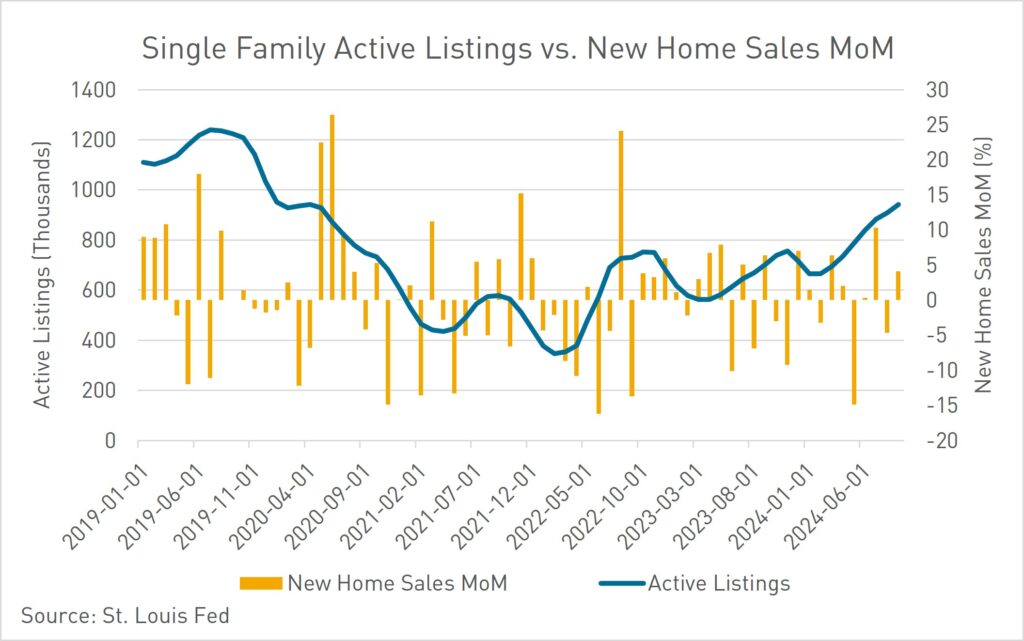

The print for U.S. previously owned home sales in September was released this week, and sales declined to an almost 14-year low as prospective buyers waited for a further decline in mortgage rates and more attractive asking prices. According to the National Association of Realtors, closings decreased 1% from a month earlier to a 3.84 million annualized rate, lower than the analyst-projected 3.88 million and forecasted to be the lowest year since the mid-1990s. The resale market has largely been stuck for the past two years, barely moving much above or below an annualized rate of 4 million homes on a monthly basis, largely due to homeowners’ reluctance to list their homes and surrender their lower mortgage rate.

The September new home sales figure, released on Thursday, exemplifies the sector’s sensitivity to interest rates. New home sales in the U.S. jumped in September as customers responded to more incentives from builders and a drop in mortgage rates. Sales of new single-family homes increased 4.1% last month to a 738,000 annualized rate, above the 720,000 analyst-estimated figure. The median home price was little changed from a year ago at $426,300, which is nearly 30% higher than at the end of 2019. Builders have been offering incentives such as discounts or mortgage rate buydowns in order to help sell homes and churn inventory.

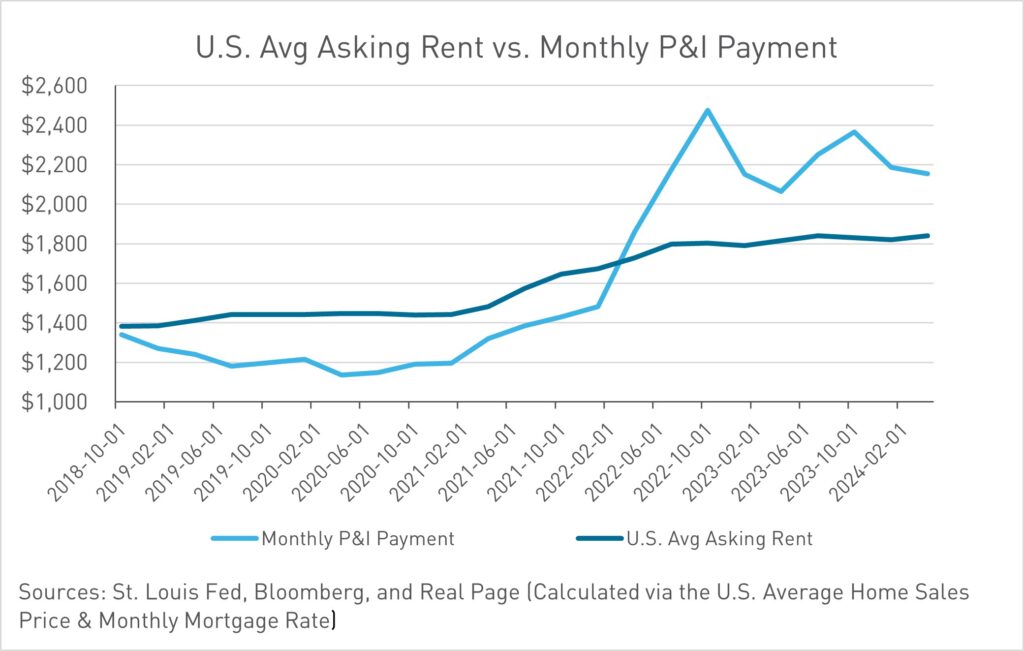

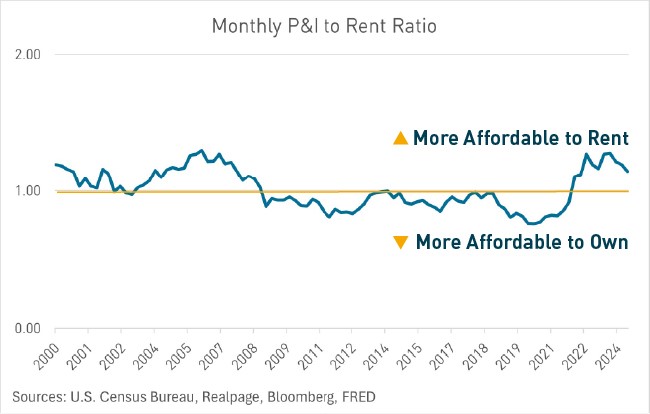

The costs between owning and renting had been relatively steady for years going into the COVID era. For much of the time following the GFC, owning was more affordable than renting. The ultra-low rates immediately following COVID drove homeownership to be at its most affordable point in decades, but skyrocketing Treasury yields and home prices quickly pushed renting to be the more affordable option in 2022. In order to move back to even, single-family rates would need to drop by almost 150 basis points. While the premium for owning a home may drop over the next few years, the confluence of rent growth, interest rate, and home price forecasts do not lend themselves to reaching that breakeven point soon.

This commentary and any statements, information, data and content contained therein, and any materials, information, images, links, sounds, graphics or video provided in conjunction with this document (collectively “Materials”) has been prepared for informational purposes or general guidance on matters of interest only, and does not constitute professional advice, advertising or a solicitation. The Materials are of a general nature and not intended to address the circumstances of any particular individual or entity. You should not act upon the information contained in the Materials without obtaining specific professional advice. As such, nothing herein constitutes legal, financial, business, investment or tax advice and you should consult your own legal, financial, tax, investment or other professional advisor(s) before engaging in any activity in connection herewith. The information in the Materials is not a substitute for a thorough due diligence investigation. No representation or warranty (express or implied) is given as to the accuracy or completeness of the information contained in the Materials, and, to the extent permitted by law, Berkadia Commercial Mortgage LLC ( together with its affiliates, the “Company”) neither accept nor assume any liability, responsibility or duty of care for any consequences of you or anyone else acting, or refraining to act, in reliance on the Materials or for any decision based on them. No part of the Materials is to be copied, reproduced, distributed or disseminated in any way without the prior written consent of the Company.