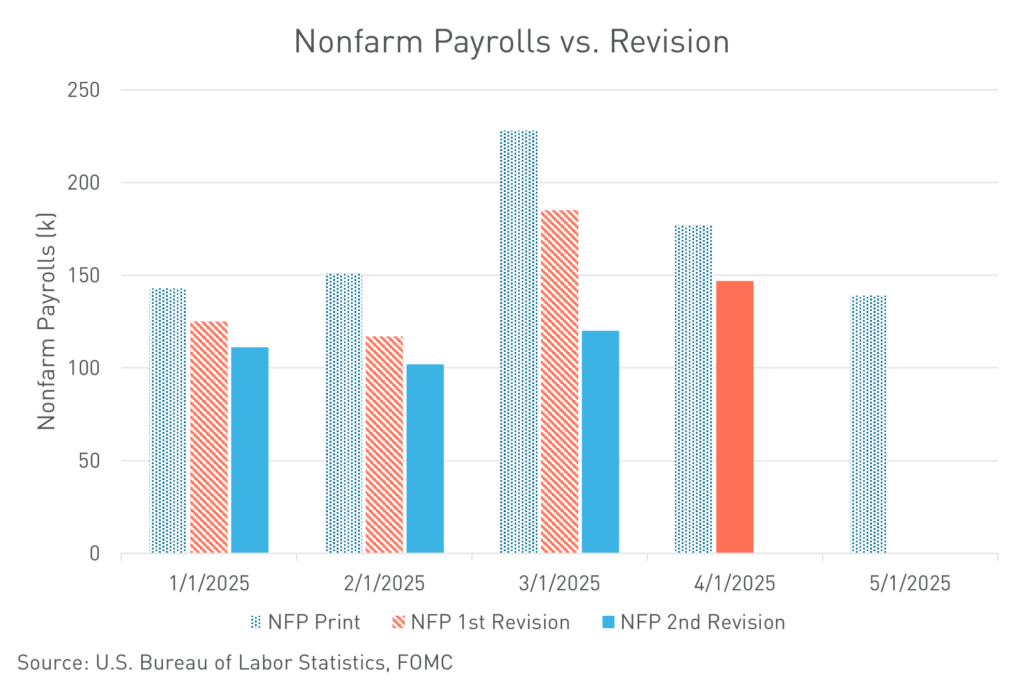

- May’s Nonfarm Payrolls print beat market expectations at 139K; unemployment rate holds steady.

- Significant downward revisions for prior months’ figures signal general weakening in the labor market.

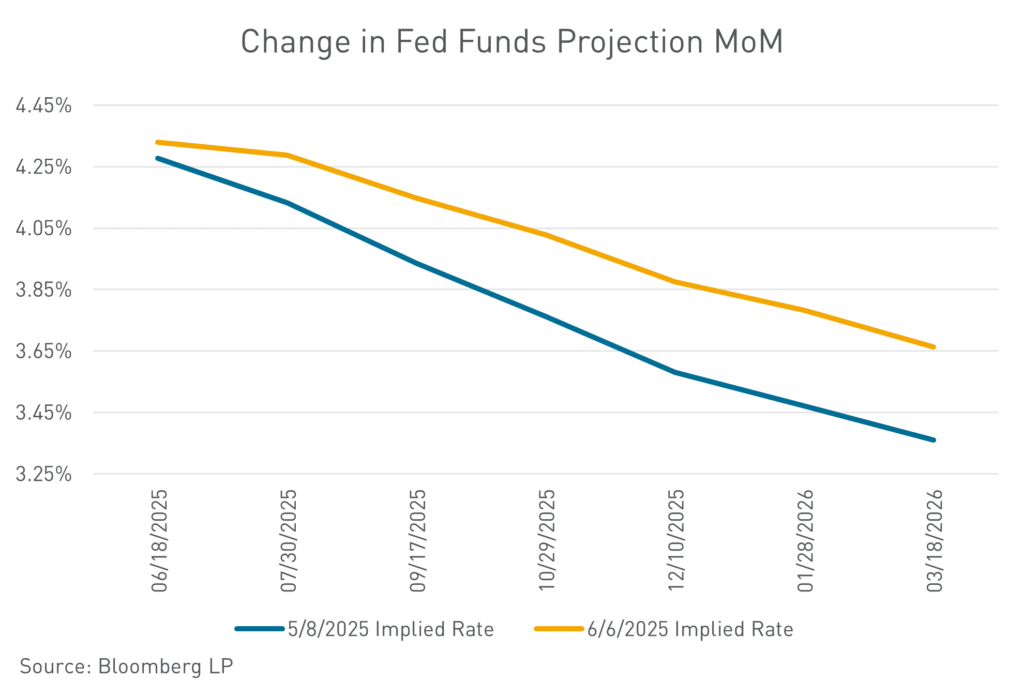

- Bond market trims expectations for rate cuts in 2025.

The May Nonfarm Payrolls and Unemployment prints were released on Friday morning—U.S. job growth moderated in May, and the prior months were revised lower. Nonfarm payrolls increased by 139,000, beating market expectations of 126,000, and the unemployment rate remained steady at 4.2%.

The payrolls figure was dual sided: the figure driven by strength at service providers, including health care and social assistance, and leisure and hospitality. The print also reflected that industries that are more exposed to tariffs flashed warning signs; manufacturing payrolls dropped 8,000 in May. Meanwhile, reflecting President Trump’s efforts to cut back on government spending, the federal government shed 22,000 jobs in May, the most since 2020.

Taking a deeper dive into the data, the labor force participation rate, which is the share of the population that is working or looking for work, fell to a three-month low of 62.4% in May. This contraction was an unusually large drop and drove the unemployment rate to hold steady. The unemployment rate was unchanged, not because jobs are plentiful, but because workers were dropping out. Notably, we continue to see downward revisions to monthly Nonfarm prints, begging the question: When will the market start taking revisions into account instead of just trading the headline number?

Friday’s figures may help temper general concerns that companies are quickly ratcheting back employment as they contend with potential higher costs related to tariffs. President Donald Trump’s decision to pause some of the more punitive import duties, including those on China, has helped lift sentiment among businesses as well as consumers. Indeed, the Consumer Confidence Board Sentiment survey rebounded from a five-month slide, approaching levels on par with pre-liberation day. Taken together, we get a conflicting picture of a weakening (but still strong) labor market and a resilient consumer. The next notable sentiment print comes on June 13 with the University of Michigan Sentiment survey, which was flirting with record lows last month.

The May Nonfarm Payrolls print did not force the Federal Reserve’s hand in upcoming monetary policy decisions. Officials have indicated they’re in no rush to cut rates until they get further clarity on the impact the administration’s policies will have on the economy—including the labor market. Market expectations assume that companies plan to pass through tariff costs to the consumer in the next two to three months. Given this expectation, the market is projecting that the Federal Open Market Committee (FOMC) is unlikely to cut rates before September, even as the job market is weakening. Market projections for rate cuts in 2025 continue to fall, with only two 25 bp cuts currently penciled in for the year, down a full 25 bps since May 1.

This commentary and any statements, information, data and content contained therein, and any materials, information, images, links, sounds, graphics or video provided in conjunction with this document (collectively “Materials”) has been prepared for informational purposes or general guidance on matters of interest only, and does not constitute professional advice, advertising or a solicitation. The Materials are of a general nature and not intended to address the circumstances of any particular individual or entity. You should not act upon the information contained in the Materials without obtaining specific professional advice. As such, nothing herein constitutes legal, financial, business, investment or tax advice and you should consult your own legal, financial, tax, investment or other professional advisor(s) before engaging in any activity in connection herewith. The information in the Materials is not a substitute for a thorough due diligence investigation. No representation or warranty (express or implied) is given as to the accuracy or completeness of the information contained in the Materials, and, to the extent permitted by law, Berkadia Commercial Mortgage LLC ( together with its affiliates, the “Company”) neither accept nor assume any liability, responsibility or duty of care for any consequences of you or anyone else acting, or refraining to act, in reliance on the Materials or for any decision based on them. No part of the Materials is to be copied, reproduced, distributed or disseminated in any way without the prior written consent of the Company.