- The FOMC voted to hold rates steady in the 4.25%–4.50% range at the March meeting

- Updated dot plot still projects two rate cuts for both 2025 and 2026

- Fed’s Summary of Economic Projections lowers expectations for GDP, increased expectations for inflation

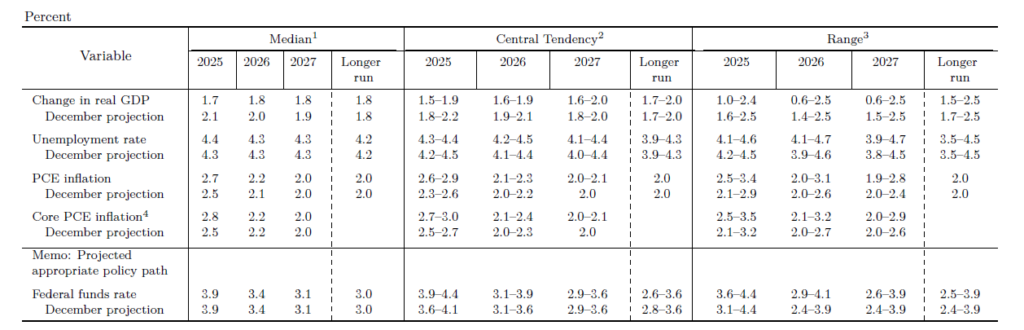

The Federal Open Market Committee (FOMC) held their March meeting on Wednesday, where committee members voted to hold the Fed funds rate steady in the 4.25%–4.50% range. The FOMC decision to hold rates steady was widely expected by the bond market, so the real headline of the meeting was the release of the Fed’s “dot plot,” which shows where committee members expect the Fed funds rate to be at the end of the calendar year. The dot plot was unchanged from the prior release in December, projecting two rate cuts in 2025 and two in 2026. Leading into the release, the market felt as though it was balanced on a knife’s edge. A hawkish pivot in the projections would likely have sent yields soaring, so a collective sigh of release could be heard when the forward rate projections came out unchanged over this year and next. However, when you look a bit more closely at the projections that comprise the dot plot, only two dots make the difference between the median dot being 50 bps of rate cuts vs. 25 bps of rate cuts, so the relief may only last until the next FOMC meeting.

Wednesday’s updated Summary of Economic Projections (SEP) unveiled the Fed’s recognition and projection of the effects that fiscal policy changes implemented by the Trump administration will have on the U.S. economy. Up until this point, Fed Chair Jerome Powell had done his best not to address any fiscal policy changes, maintaining his stance that the Fed will be data dependent while making monetary policy decisions. The SEP reflected an upward projection for inflation in 2025 and 2026, but the 2027 and long-term projections remained flat.

Click here to view the full table

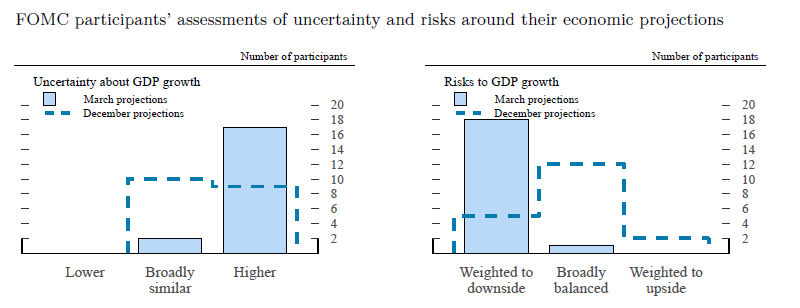

At Wednesday’s press conference, Powell highlighted that some measures of inflation expectations have moved up, but that beyond the next year or so, “most” measures of longer-term expectations remain consistent with the Fed’s 2% target. When Powell was asked about the revision to inflation forecasts and how much of it is due to tariffs, he noted that it’s hard to parse how much of inflation is driven by tariffs, but that they’re going to try to figure this out. “Clearly, some of it—a good part of it—is coming from tariffs,” Powell said, and added that the “base case” for tariff-fueled inflationary pressures will be transitory. The updated SEP also reflected that more FOMC participants are now concerned about uncertainty surrounding the economy. Most see risks to GDP as weighted to the downside now, and those to unemployment and inflation weighted to the upside. The updated SEP lowered GDP projections to 1.7% in 2025, down from 2.1% prior.

When called to defend lower growth and higher inflation, Powell was clear that the economy is healthy. He attributed negative sentiment to the turmoil of a new administration that is making big changes in policy but firmly reiterated that the economy is healthy. The hard data supports a good economy, but the soft data (read: surveys) are negative. The Fed acts on hard data. The most recent Consumer Price Index (CPI) and Personal Consumption Expenditures (PCE) inflation prints both noted cooling inflation from the month prior. Unemployment remains low, and recent nonfarm payrolls prints have been steadfast. Until either the labor market or inflation veers off track, the Fed will continue to hold rates steady and analyze the data.

While this meeting did have a bit of a “kick-the-can” feeling until the Fed’s May meeting, it does leave the rates market in a positive place. In leaving rate cuts in the forecast and acknowledging the transitory impact of tariffs on inflation, the Fed leaves a believable way forward to reduce the federal funds rate. This also allows support for the longer end of the curve to stay in the range-bound trading pattern we’ve seen over the last several weeks, hovering mostly in the 4.20%–4.40% range, at least until we receive some news that will jolt us out of the status quo.

This commentary and any statements, information, data and content contained therein, and any materials, information, images, links, sounds, graphics or video provided in conjunction with this document (collectively “Materials”) has been prepared for informational purposes or general guidance on matters of interest only, and does not constitute professional advice, advertising or a solicitation. The Materials are of a general nature and not intended to address the circumstances of any particular individual or entity. You should not act upon the information contained in the Materials without obtaining specific professional advice. As such, nothing herein constitutes legal, financial, business, investment or tax advice and you should consult your own legal, financial, tax, investment or other professional advisor(s) before engaging in any activity in connection herewith. The information in the Materials is not a substitute for a thorough due diligence investigation. No representation or warranty (express or implied) is given as to the accuracy or completeness of the information contained in the Materials, and, to the extent permitted by law, Berkadia Commercial Mortgage LLC ( together with its affiliates, the “Company”) neither accept nor assume any liability, responsibility or duty of care for any consequences of you or anyone else acting, or refraining to act, in reliance on the Materials or for any decision based on them. No part of the Materials is to be copied, reproduced, distributed or disseminated in any way without the prior written consent of the Company.