U.S. ECONOMIC MACRO COMMENTARY & INSIGHTS

- FOMC holds rates steady at May meeting

- Updated dot plot projects one rate cut this year

- Recent inflation prints have the market fading the Fed’s projections

The Federal Open Market Committee (FOMC) held their June meeting on Wednesday this week, where committee members unanimously voted to hold the benchmark rate steady in the 5.25%-5.50% range. For a seventh straight meeting, the FOMC’s statement repeats language stating that the committee doesn’t expect to cut rates “until it has gained greater confidence that inflation is moving sustainably toward 2%.” This sentiment was reiterated in the Fed’s dot plot; the updated projections were a hawkish surprise for investors, forecasting only one rate cut this year. FOMC median forecast shows 25 bps of rate cuts in 2024, down from the previous projection of 75 bps, and the FOMC median forecast for 2025 projects 100 bps of cuts, up from the previous projection of 75 bps. Powell doubled down on the dot plot’s hawkish tone at the press conference, proclaiming, “If the economy remains solid and inflation continues to persist, we are prepared to maintain the current rate level. If the labor market were to weaken significantly…we are prepared to respond. We are pursuing both sides of our dual mandate – max employment and stable prices.”

06.12.24 FOMC DOT PLOT

Powell slightly downplayed the importance of the dot plot, saying he doesn’t have high confidence in the forecasts for rates, and that each of the individual forecasts are plausible. Inflation projections in the Fed’s Summary of Economic Projections were moved up, from 2.6% up to 2.8%, which could be a result of the rolling off of super-low immaculate disinflation numbers of 12 months ago, or could be a nod to the Fed accepting slightly higher inflation as a tradeoff for sticking a soft landing.

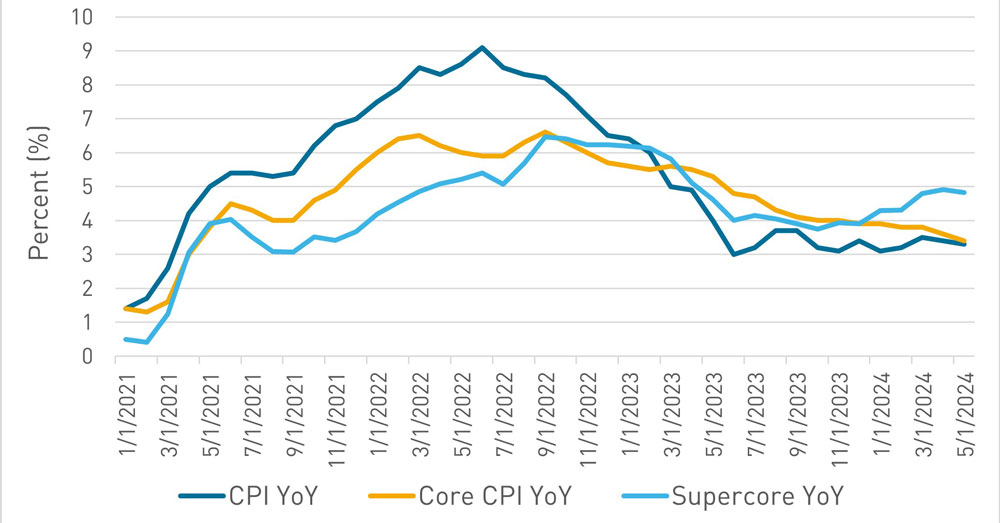

Despite the hawkish dot plot, the market continues to price in two rate cuts for 2024. On Wednesday morning, prior to the Fed announcement, the May Consumer Price Index (CPI) print was released. The CPI print was essentially flat from the month before and up 3.3% from one year ago, down from April’s 3.4%. Core CPI, which excludes volatile food and energy items, rose 0.2% in May and was up 3.4% from a year ago. Both measures of inflation were softer than economists predicted.

Historical Consumer Price Index (CPI)

Market optimism has continued despite last Friday’s Nonfarm Payrolls (NFP) print. The NFP print was significantly above market expectations, 272K vs 180K projected. The print caused a sell-off in Treasury rates; the 10-year UST climbed 15 bps intraday but has since rallied back to tighter levels than those seen before the payrolls number. Given that the labor market remains strong and inflation remains around levels seen a year ago, the Fed is proceeding with caution. Enda Curran, a Bloomberg Global Economy reporter, sums up Powell’s sentiment: “Powell is being careful not to reverse pivot the un-pivot of the pivot he signaled in December. He wants everyone to know that today’s inflation reading is hopeful, but there is a way to go yet.”

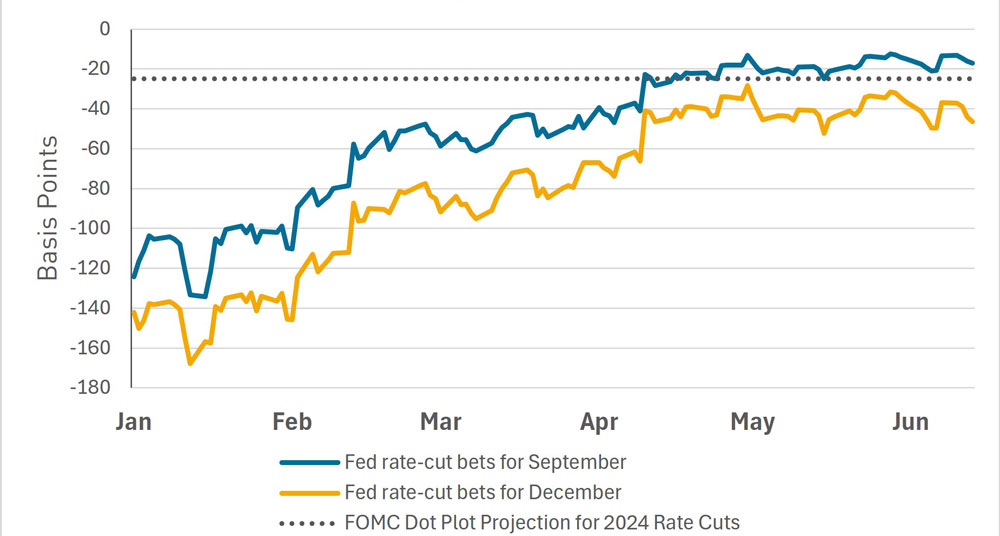

Rate-Cut Bets for September and December ’24

According to Bloomberg, the market is currently pricing in a 65% chance of a rate cut at the September FOMC meeting. Committee members have a number of economic releases to consider before the September meeting, including three nonfarm payrolls prints, three CPI releases, and three Personal Consumer Expenditures (PCE) data points. Given the highly anticipatory nature of the market, and the Fed’s guiding principle of data dependence, Treasury rate volatility should be expected surrounding these upcoming releases.

This commentary and any statements, information, data and content contained therein, and any materials, information, images, links, sounds, graphics or video provided in conjunction with this document (collectively “Materials”) has been prepared for informational purposes or general guidance on matters of interest only, and does not constitute professional advice, advertising or a solicitation. The Materials are of a general nature and not intended to address the circumstances of any particular individual or entity. You should not act upon the information contained in the Materials without obtaining specific professional advice. As such, nothing herein constitutes legal, financial, business, investment or tax advice and you should consult your own legal, financial, tax, investment or other professional advisor(s) before engaging in any activity in connection herewith. The information in the Materials is not a substitute for a thorough due diligence investigation. No representation or warranty (express or implied) is given as to the accuracy or completeness of the information contained in the Materials, and, to the extent permitted by law, Berkadia Commercial Mortgage LLC ( together with its affiliates, the “Company”) neither accept nor assume any liability, responsibility or duty of care for any consequences of you or anyone else acting, or refraining to act, in reliance on the Materials or for any decision based on them. No part of the Materials is to be copied, reproduced, distributed or disseminated in any way without the prior written consent of the Company.