- FOMC unanimously voted to hold rates steady at the May meeting

- Fed’s announcement makes key statement: “Uncertainty about the economic outlook has increased further.”

- Inflation continues to cool as labor market remains solid

The Federal Open Market Committee (FOMC) held its meeting on Wednesday, May 7. The committee unanimously voted to hold rates steady in the 4.25%–4.50% range. The decision to hold rates steady was widely expected by the market—analysts instead focused on any future guidance that Fed Chair Jerome Powell might provide on upcoming monetary policy. In the shadow of President Trump’s ongoing tariff negotiations, the Fed is content with waiting to see how things play out, citing that “uncertainty about the economic outlook has increased further.” At the press conference following the Fed’s announcement, Powell used some version of the word “wait” 22 times to underscore how the Fed isn’t in a rush. “The costs of waiting to see further are fairly low, we think, so that’s what we’re doing,” Powell said.

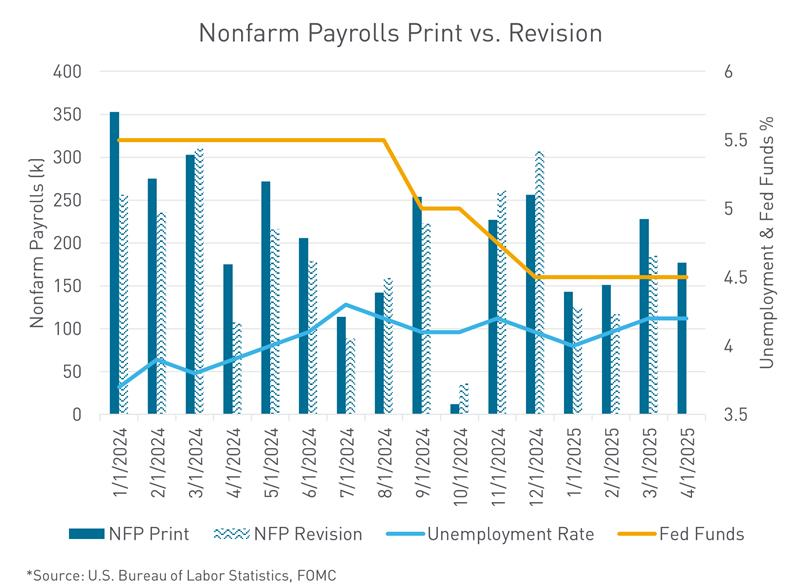

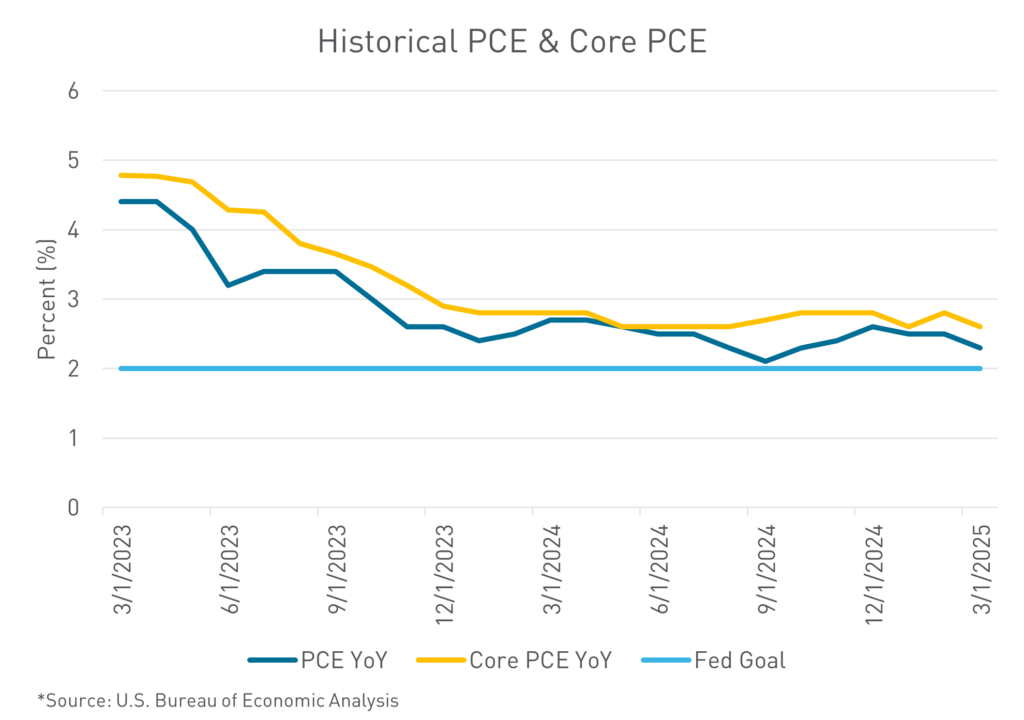

While the Fed continues to reiterate its focus on the dual mandate, it will take movement in the labor market to spur rate cuts. While the headline number for Nonfarm Payrolls is driving expectation, the downward revisions in the first quarter need to be taken into account and are signaling that there may not be as much strength in the labor market as the Fed is conveying by calling it “broadly in balance.” The Fed’s statement went out of its way to reinforce that the unemployment rate has stabilized and the labor market is solid. On the pricing mandate, Powell noted that inflation remains “somewhat elevated.” The latest Personal Consumption Expenditures (PCE) price gauge showed a constructive 0% monthly change for the core measure, but 2.6% on a year-on-year basis; these levels are still above the 2% target. Powell addressed the recent negative first-quarter Gross Domestic Product (GDP) print by noting the significant imbalance between imports and exports caused by the front-running of purchases before impending tariffs.

The implication of impending tariffs was a core theme of the post-announcement press conference. Powell said the effect of tariff hikes on the economy remains highly uncertain, but if the announced increases were to be sustained, that would impact inflation, growth, and employment. Powell stated that tariffs, if sustained, “are likely to generate a rise in inflation, a slowdown in economic growth, and an increase in unemployment,” but “the effects on inflation could be short lived, reflecting a one-time shift in the price level.” He added, “It is also possible that the inflationary effects could instead be more persistent. Avoiding that outcome will depend on the size of the tariffs’ effects, on how long it takes for them to pass fully into prices, and ultimately, on keeping longer-term inflation expectations well anchored.” When asked which side of the mandate will need addressing first, higher inflation or unemployment, Powell said that both risks have gone up, and it isn’t clear which one will be the bigger concern, adding, “It’s too early to know.”

The Fed finds itself in a nearly untenable position where its two mandates are likely to diverge, influenced by highly unpredictable government policy. One underrated moment in the press conference had to do with why the Fed isn’t acting on the sentiment data. There has been much press about how quickly consumer sentiment has turned, and that the Fed should lean in as a leading indicator. The Fed was quite clear that the link between sentiment data and consumer spending has been weak over several years. The Fed will continue to be data-dependent in making future monetary policy decisions. Powell noted that current policy is modestly or moderately restrictive, and that he believes that the Fed is in a solid position to pivot monetary policy should the data begin to skew in one direction or another.

This commentary and any statements, information, data and content contained therein, and any materials, information, images, links, sounds, graphics or video provided in conjunction with this document (collectively “Materials”) has been prepared for informational purposes or general guidance on matters of interest only, and does not constitute professional advice, advertising or a solicitation. The Materials are of a general nature and not intended to address the circumstances of any particular individual or entity. You should not act upon the information contained in the Materials without obtaining specific professional advice. As such, nothing herein constitutes legal, financial, business, investment or tax advice and you should consult your own legal, financial, tax, investment or other professional advisor(s) before engaging in any activity in connection herewith. The information in the Materials is not a substitute for a thorough due diligence investigation. No representation or warranty (express or implied) is given as to the accuracy or completeness of the information contained in the Materials, and, to the extent permitted by law, Berkadia Commercial Mortgage LLC ( together with its affiliates, the “Company”) neither accept nor assume any liability, responsibility or duty of care for any consequences of you or anyone else acting, or refraining to act, in reliance on the Materials or for any decision based on them. No part of the Materials is to be copied, reproduced, distributed or disseminated in any way without the prior written consent of the Company.