- Treasury rates drop to their lowest point since mid-December

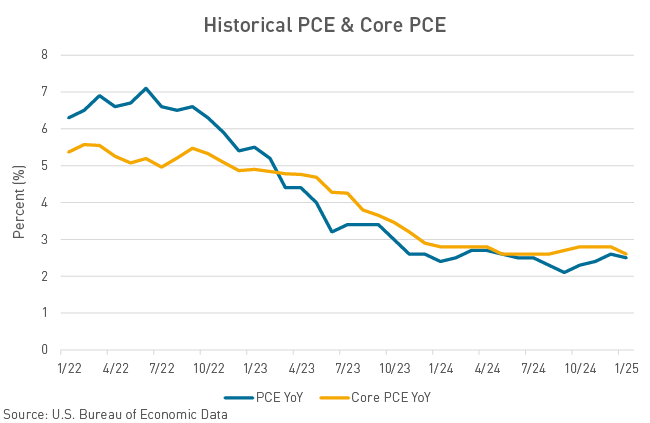

- January’s Personal Consumption Expenditures (PCE) gauge cooled year over year

- Volatility persists in the bond market

Treasury yields slid to their lowest levels of the year on Friday as recent economic prints suggest a cooling U.S. economy. The Fed’s preferred inflation gauge, Personal Consumption Expenditures (PCE), was released on Friday morning and eased fears of inflation reigniting in the short term. The core PCE index rose 0.3% from December and 2.6% from last year, matching the smallest annual increase since early 2021. Inflation-adjusted consumer spending fell 0.5%, marking the biggest monthly decline in almost four years, driven by a decline in motor vehicle purchases and slowing services spending. The 10-year Treasury rate dropped to 4.25%, well below its recent 4.80% January peak, as market analysts price in a second rate cut in 2025.

Treasury yields made a sharp pivot lower in mid-February following the January CPI print. The headline CPI rose 0.5% last month, the most since August 2023, led by a range of household expenses like groceries and gas. This print marked the recent high in Treasury yields. However, the next-day U.S. retail sales print hit the skids in January, falling by the most in almost two years, signaling a consumer spending pullback from the excesses of the 2024 holiday season. Month-over-month retail sales fell by 0.9% from the previous month’s positive 0.7%. Additionally, consumer sentiment fell for the second consecutive month as near-term inflation views rose sharply. Recent economic prints have continued to put downward pressures on Treasury yields since the consumer sentiment figure. To recap:

- 2/14 – In a dramatic reversal of Wednesday’s post-CPI losses, Treasuries ended 5-11bps richer on Thursday after details of the PPI report came out relatively benign.

- 2/20 – Dovish FOMC Minutes suggest the possibility of pausing/slowing QT ahead of potential debt ceiling turmoil sent U.S. Treasury yields 0-2bps lower.

- 2/21 – Assurance from Treasury Secretary Bessent that increasing the share of longer-term U.S. Treasury issuance was “a long way off” drove yields tighter on Thursday, alongside a meaningful selloff in USD throughout the day.

- 2/25 – Data released showed the Conference Board’s consumer confidence index fell more than expected, landing at the lowest level since June.

- 2/26 – An intensification of growth slowdown fears saw Treasuries extend recent gains, rallying 6-10bps across the curve to reach year-to-date lows in yield alongside a flight-to-quality selloff in various risk assets. A weak consumer confidence report, strong 5-year auction, Bessent reiterating his confidence that 10-year yields would “naturally come down,” and a wave of short covering flows from a variety of accounts throughout the day exacerbated the price action.

- 2/28 – PCE dashed fears of inflation reigniting in the short term.

Friday’s PCE print offered some relief to the market after a string of reports suggested price pressures are heating up – particularly after the January CPI figure increased for the fourth straight month, posting the highest headline print since August of 2023. The PCE report eased tensions on the inflation front, but ongoing price pressures and policy changes, including new tariffs, may weigh on the consumer and impact inflation expectations. The core PCE index, which excludes food and energy items, rose 0.3% on a monthly basis and increased 2.6% year over year, matching the smallest annual increase since early 2021. Inflation-adjusted consumer spending fell 0.5%, marking the biggest monthly decline in almost four years amid winter weather after a robust holiday season. Fed officials have indicated they need to see a meaningful easing in inflation before they begin lowering interest rates again, especially when they factor in the uncertainty around how President Donald Trump’s policies will impact prices. The string of economic prints over the second half of February has caused the market to price in a second rate cut in 2025 – the first in June and the second in October.

The surge in volatility we experienced during the will-they, won’t-they rate-hiking cycle that began in 2022 has abated somewhat. The MOVE Index measures volatility on a basket of 2-year, 5-year, 10-year, and 30-year constant maturity Treasury securities, and provides an excellent gauge of bond market volatility (think VIX but for bonds). We recently hit multi-year lows on the MOVE Index, which is comforting only if you look at the last several years. When you expand your view over the past decade, the current lows in volatility we are experiencing would be roughly equal to the high watermark of the previous period. Barring unexpected Fed action, this feels like the new normal when it comes to rate volatility. To put numbers to that, 30% of trading days this year have had an intraday swing of 10 bps or more, so the new normal is still quite volatile. While this may be our new normal, look for larger swings leading into March’s FOMC meeting, and position your deals accordingly.

This commentary and any statements, information, data and content contained therein, and any materials, information, images, links, sounds, graphics or video provided in conjunction with this document (collectively “Materials”) has been prepared for informational purposes or general guidance on matters of interest only, and does not constitute professional advice, advertising or a solicitation. The Materials are of a general nature and not intended to address the circumstances of any particular individual or entity. You should not act upon the information contained in the Materials without obtaining specific professional advice. As such, nothing herein constitutes legal, financial, business, investment or tax advice and you should consult your own legal, financial, tax, investment or other professional advisor(s) before engaging in any activity in connection herewith. The information in the Materials is not a substitute for a thorough due diligence investigation. No representation or warranty (express or implied) is given as to the accuracy or completeness of the information contained in the Materials, and, to the extent permitted by law, Berkadia Commercial Mortgage LLC ( together with its affiliates, the “Company”) neither accept nor assume any liability, responsibility or duty of care for any consequences of you or anyone else acting, or refraining to act, in reliance on the Materials or for any decision based on them. No part of the Materials is to be copied, reproduced, distributed or disseminated in any way without the prior written consent of the Company.