• It’ll be slower going lower. Have we entered “The Pause?”

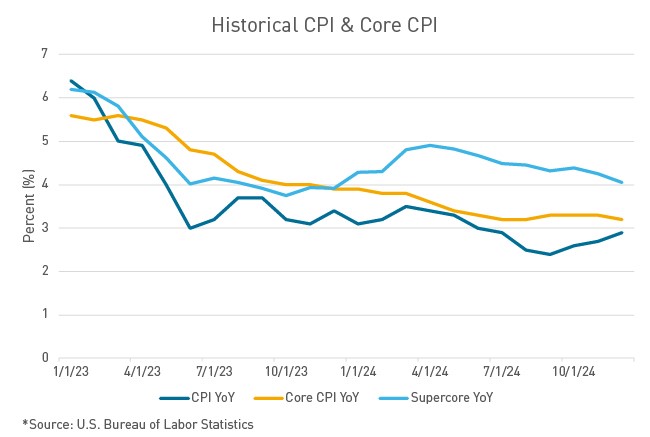

• December Core CPI print eases from the month prior, a positive sign for markets.

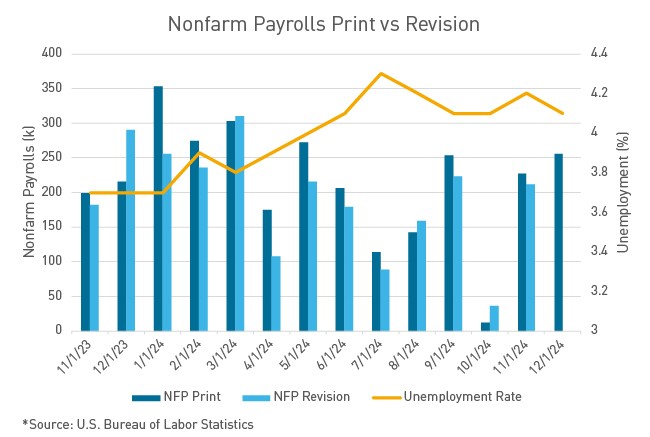

• Strong nonfarm payrolls and unemployment prints show that the labor market has found its footing.

The Fed is entering the new year with a fresh slate on macroeconomic policy. Gone are the days of the “hard landing” or “soft landing”—those are being left in 2024. We’ll now move from flying analogies to sports analogies and label the Fed in “Ready Position.” Pretty much every sport has a ready position, where you’re balanced and poised to react quickly, which is exactly how the Fed is set up this year. Whether it’s inflation information, labor data, or financial conditions, the Fed is well positioned to react in a way that allows them to cut, hike, or hold rates steady while reacting to real-time data.

The Fed successfully eased the economy out of the Covid-era pricing pressures without outright tanking the economy. After years of monetary policy adjustments, inflation has cooled significantly, the labor market remains resilient, and the Fed’s “plane” has finally landed. Following the rate cut at the December Federal Open Market Committee (FOMC) meeting, the Fed is poised to hold rates steady and see how things play out. Recent economic prints have given FOMC members confidence that both sides of their dual mandate—price stability and maximum employment—are roughly in balance at current rate levels. Current projections show a 3% chance of a rate cut at the January FOMC meeting, according to Bloomberg.

Both the Fed and the market celebrated on Wednesday morning when the December Consumer Price Index (CPI) print was released. U.S. consumer prices rose less than the market forecast in December, driven by cheaper hotel fares, smaller medical care service charges, and notably, tame rent increases. Shelter prices, the largest category within services, climbed 0.3% in December for a second month. Owner’s Equivalent Rent as well as Rent of Primary Residence (both subsets of shelter) ticked up following the smallest gains since 2021. The core CPI, which excludes food and energy prices, increased by 0.2% month over month, marking the first step down in six months. After months of elevated prints, the easing CPI print helps Fed officials gain confidence that progress on taming inflation to the 2% goal has resumed.

The December nonfarm payrolls and unemployment prints, released last Friday, also provided FOMC members with firm confidence that the U.S. economy is in a strong position to start the new year. The U.S. economy added 256,000 jobs in December, and the unemployment rate decreased to 4.1%, a decrease from 4.2% the month prior. Last month’s payroll gain was the largest since March, and well above the 155,000 jobs that economists had expected. The strong jobs reports have reduced any lingering concern of weakening. While the feeble labor market prints in the third quarter of 2024 may have prompted the Fed to begin cutting rates, the labor market has proven to be stronger than once feared.

Labor market stability, paired with mixed progress on inflation, has clouded the outlook for future rate cuts. Federal Reserve Governor Christopher Waller spoke on Thursday and suggested that the FOMC could lower interest rates again in the first half of 2025 if inflation data continues to be favorable. He added that he wouldn’t entirely rule out a cut in March. Waller believes that if future inflation figures fall in line with December’s positive report, the Fed may cut rates more this year and sooner than investors are currently expecting. “I’m optimistic that this disinflationary trend will continue, and we’ll get back closer to 2% a little quicker than maybe others are thinking,” Waller said. The Fed’s decision on rate cuts will depend on incoming data, and for now, they will remain nimble with their policy decisions.

This commentary and any statements, information, data and content contained therein, and any materials, information, images, links, sounds, graphics or video provided in conjunction with this document (collectively “Materials”) has been prepared for informational purposes or general guidance on matters of interest only, and does not constitute professional advice, advertising or a solicitation. The Materials are of a general nature and not intended to address the circumstances of any particular individual or entity. You should not act upon the information contained in the Materials without obtaining specific professional advice. As such, nothing herein constitutes legal, financial, business, investment or tax advice and you should consult your own legal, financial, tax, investment or other professional advisor(s) before engaging in any activity in connection herewith. The information in the Materials is not a substitute for a thorough due diligence investigation. No representation or warranty (express or implied) is given as to the accuracy or completeness of the information contained in the Materials, and, to the extent permitted by law, Berkadia Commercial Mortgage LLC ( together with its affiliates, the “Company”) neither accept nor assume any liability, responsibility or duty of care for any consequences of you or anyone else acting, or refraining to act, in reliance on the Materials or for any decision based on them. No part of the Materials is to be copied, reproduced, distributed or disseminated in any way without the prior written consent of the Company.